My Journey in Finance: The Momentum Crash

Disclaimer: Your capital is at risk. This is not investment advice.

This series introduces my experiences with momentum investing. I kicked off with Why Momentum Works, then How to Build a Momentum Fund, and last week, Riding the Escalators. Please take a look at these before you continue.

So far, we have covered the basics of momentum investing, a form of trend-following that focuses on the market leaders. Over the long term, it is a strategy that has beaten the market handsomely, but not without fright. In this piece, I shall show you what happens when it all goes wrong.

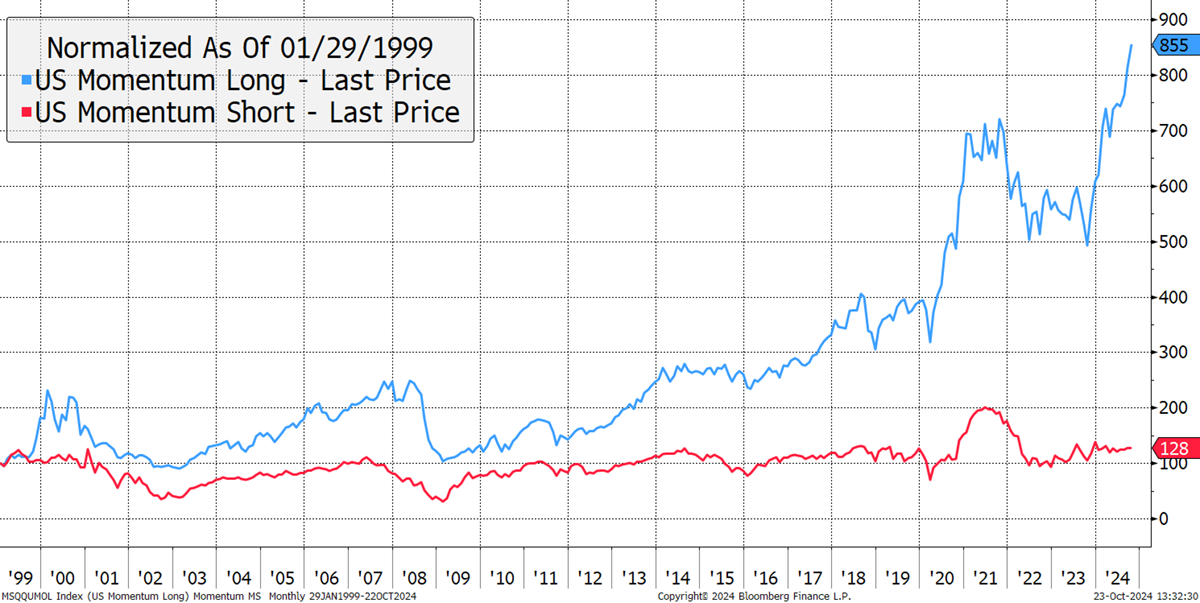

Not only does the market have winners, the best-performing stocks (blue), but it also has losers, the worst-performing stocks (red). There are important lessons from both groups. The winners are measured by past 12-month performance (with filters), and the losers are the stocks that fared the worst. In recent years, Morgan Stanley created indices to measure this, and I show them from 1999.

Past Winners and Losers

These indices were created after the credit crisis, and I would guess in or around 2015. That means the data calculated beforehand was a backtest, intended to recreate the past. In my opinion, the dotcom boom and bust from 1999 to 2002 is likely understated by this data, as many stocks went to the moon and back (Pets.com and so on). It certainly felt crazier at the time than this data shows. I am not criticising the data, merely stating how difficult it is to get accurate historical market data, especially in the olden days. These days, record-keeping is much improved. As a result, I think the last ten years, which used actual market data, are likely to more accurately reflect the momentum effect in the US stockmarket.

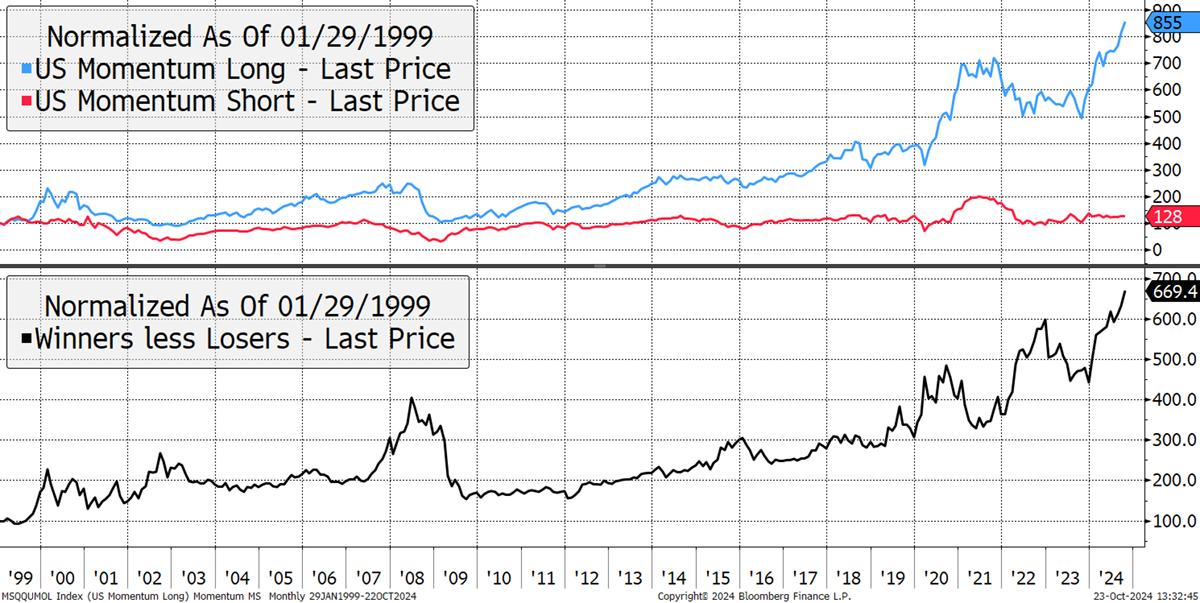

The winners have beaten the bull markets but, on occasion, they have suffered great losses. The losers never seem to do much but spring to life during the momentum crashes. The lower black line shows the difference between the winners and the losers and measures the momentum effect (momo). That is essentially what a hedge fund that bought the winners and sold the losers short would look like.

The Winners Don’t Always Win

I highlight this by looking at momo and the market (S&P 500) together. The key point here is that when the market emerges from a bear, the momo crashes, as highlighted. This happened in 2002, 2009, 2016, 2020 and 2022.

Five Momentum Crashes

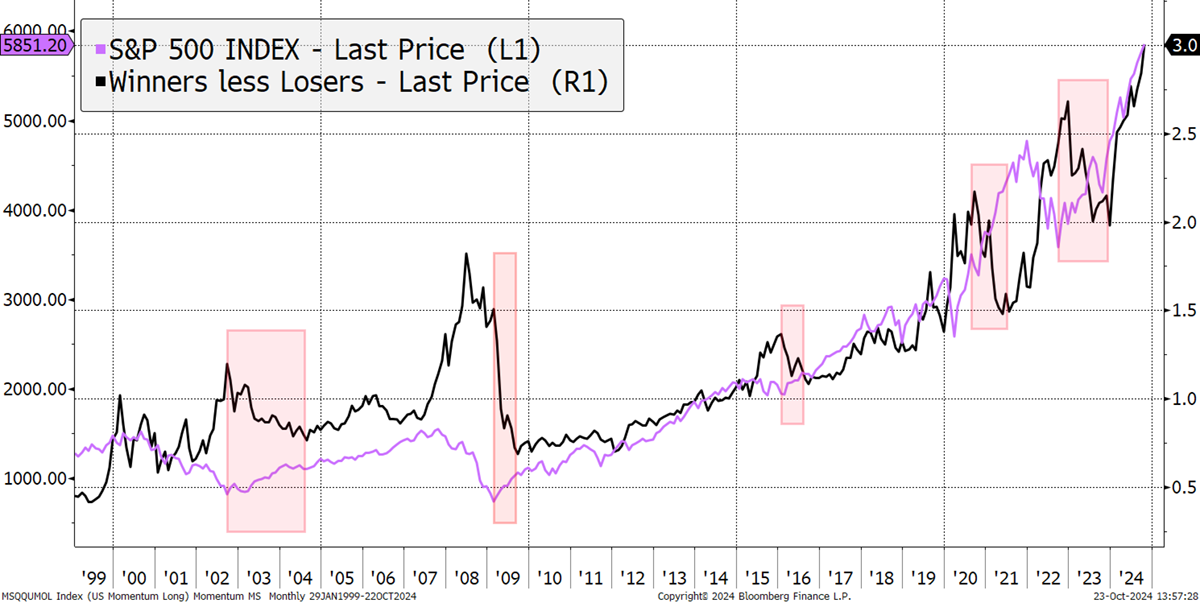

What is typical is that the winners offer sanctuary after the bear market begins and offer shelter during the market fall. Then, when the market finally bottoms, the losers lead the rally while the winners stall. The reversal of momo can be dramatic and sudden. Investors holding the winners at the time, proud of their outperformance during a bear market, complain that the “trash” is rallying, and it isn’t right. What’s happening is that the losers are heavily oversold compared to the market, while the winners are crowded. The market normalises, and that’s the set-up for a momentum crash.

This is a fabulous time to buy the past losers, as The Multi-Asset Investor clients have experienced several times. It is the safest time to buy oversold value stocks with ugly price charts. The rally starts with short covering before continuing as the economy starts to improve. All the while, the old winners remain crowded and fail to participate in the rally.

Zooming in on momo using a log scale, this data shows a 4.3% trend growth rate for the winners versus the losers going back 25 years. What’s clear is how, in 2008, ahead of the credit crisis, the momo move was extreme. This is a fact few understood at the time because there were no publicly available momo indices, just a few academic papers that recorded the experiences from the 1970s.

Momentum Crashes

Starting in mid-2008, momo fell from above the upper band to the lower band over a 15-month period. It was a momo crash of historical proportions, much greater than the other four highlighted above. The bigger the market crash, the bigger the momo crash that follows. In 2009, momo fell by 62%.

It is notable that momo has been choppy of late, with several smaller crashes (compared to the crash in 2008) in quick succession. Having embraced momo in the past, I felt it was overdone in late 2020. Value had faced years of underperformance against growth, and it was time to rotate (red circle). That worked well into late 2022 but has reversed since.

Value versus Growth

In 2024, so many indicators warn of the dangers of pursuing growth stocks in this market regime, notably valuations, which I have written much about. The concentration of a few richly valued companies makes the whole idea of chasing growth uncomfortable. But we know what happened after the dotcom era. Investing went back to normal for a while, and it was all about PEs, cash flow and dividends. It may sound dull compared to AI and space travel, but fundamental investing works.

More to the point, the popular momo funds available, such as the Global Momentum ETF by iShares, have failed to keep up with the market since my concerns in September 2020. The strategy is based around momentum and market cap. While they held the big tech stocks, with, say, 20% or 30% of their allocation, the other 70% or 80% has weighed them down. Chasing the past years’ trends hasn’t been a particularly profitable strategy for the past four years compared to the market. Momo has been strong, but the market has been even stronger. The purple momo-relative line has yet to make a new high since September 2020.

MSCI Global Momentum Index versus the World Index

This strategy has been whipsawed time and again. In 2022, it had been adding oil and cutting technology, only for the situation to quickly reverse. It’s harsh but true, but this era of money printing hasn’t been kind to momo, but it has been a boon for the index.

Next week, I’ll spill the beans on my global trend fund that I launched on 5th May 2005. It was one hell of a ride.

A Week at ByteTree

It’s the end of the month, and Robin and Rashpal returned with their latest monthly Adaptive Asset Allocation Report. In “Contest but no Victory”, their proprietary AAA model continues to rank equities as the strongest trending assets, which has reinforced their stance to remain invested despite the growing uncertainty worldwide. They also note that China has made the biggest move by far, leaping 18 positions on the table, which has reignited interest in Emerging Markets. Gold also tops the AAA model alongside equities, remaining a reliable hedge during market uncertainty.

In The Multi-Asset Investor, I celebrated my 100th issue published on ByteTree.com. As this publication was a continuation of my time writing The Fleet Street Letter at Southbank, the actual issue number is closer to 400, but I’ve lost count. Fit for the occasion, I added a company with an impressive long-term track record to the Whisky portfolio. It’s been on my watch list for well over a year, and the time to add it has finally arrived. 100 issues – I hope to write 1000 more.

In Venture, I made a new recommendation for an impressive and resilient company that has been fighting for survival and has turned the corner.

In ByteFolio, the analysts gave an inside look at meme coins. Love them or hate them, meme coins have skyrocketed in popularity, and a few of them now reside within the top 100 crypto tokens by market cap. The appeal is baffling, so we reached out to an expert in the space to better understand what the drivers are.

Finally, in Token Takeaway, Ali looked at Raydium and its native token, RAY. Raydium is the largest, fully decentralised exchange on Solana, having enjoyed an astronomical rise in popularity over the past year. Launched in early 2021, Raydium now ranks as the 4th largest protocol across the whole DeFi sector in terms of liquidity. Impressive – it clearly pays to be associated with the most rapidly growing chain in the crypto ecosystem.

The latest BOLD rebalancing report will be delivered tomorrow (Monday). It’s been a strong month.

Have a great weekend,

Charlie Morris

Founder, ByteTree