My Journey in Finance: Riding the Escalators

Disclaimer: Your capital is at risk. This is not investment advice.

This series introduces my experiences with momentum investing. I kicked off with Why Momentum Works and, last week, How to Build a Momentum Fund. Please take a look at these before you continue.

There are many effective equity investment strategies such as quality (great companies over the long term), value (undervalued companies that get re-priced) and events (a catalyst for change). They all have their merits, and I intend to cover these areas and more, but momentum is a hot topic, and that’s why I’m covering it first. At times it can be powerful, but at other times, brutal.

The reason the winning stocks can be so powerful is that investors can smell growth, which causes the shares to rise. It then sees more growth, and a positive feedback loop ensues. George Soros called this his Theory of Reflexivity. Most of us call it a bubble because, eventually, it will burst. But as Soros famously said, “If I see a bubble forming, I rush in to buy.”

In a go-go market, a company’s share price can rise faster, sometimes much faster, than the company’s growth. The idea is that should the growth continue, the shares will be worth much more in the future, so why wait until then, when we can bid them up now? It is the same school of thought that gives the leading strikers an inelastic valuation (see part 1) while ignoring the price paid per goal. Or, in Buffett-speak, the voting machine versus the weighing machine.

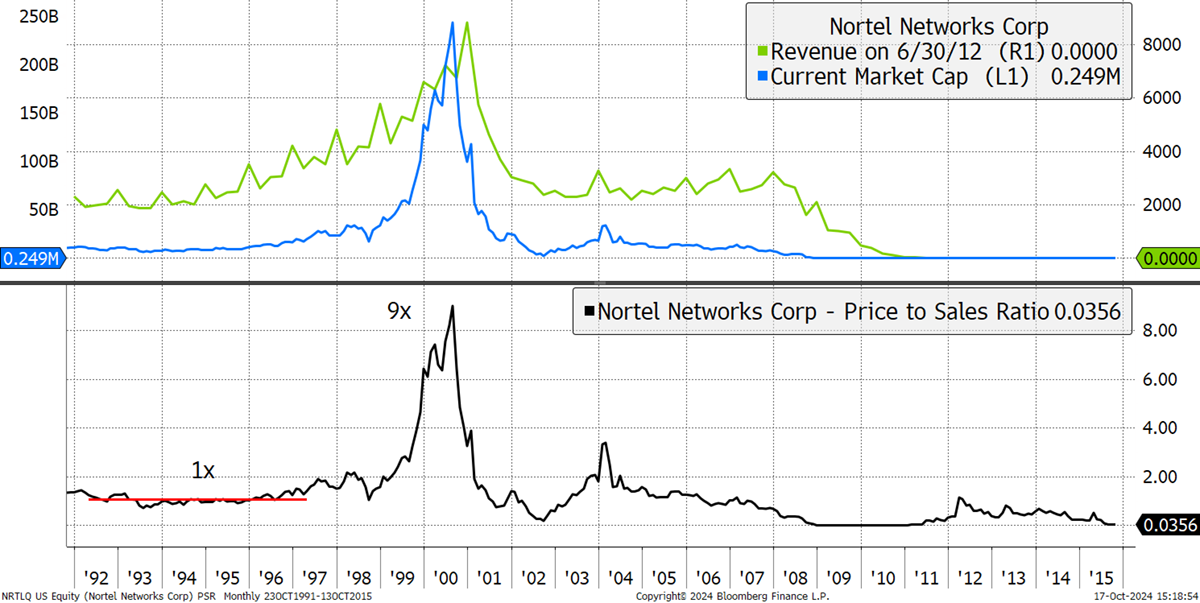

I will go through a few examples of some of the challenges that a well-managed momentum fund faces. Canada’s Nortel Networks was a good example. In the year 2000, it was briefly worth $243 billion, making it one of the most valuable companies in the world at the time. It didn’t grow in the early 1990s, but then in 1995 it delivered 20% growth for the next three years, and then the fun began. It had acquired Germany’s Bay Networks in 1998, a competitor to Cisco, and the market went wild. At the time, servers were all the rage because they enabled the internet.

The lower line (black) shows Nortel’s price-to-sales ratio (PSR). It traded at 1x sales in the mid-1990s, only to surge to 9x sales by 2000. Then sales fell as the internet boom stalled, and the scramble for the exit was painful, with a 33% drop in February 2001 in a single trading day. It demonstrates how things can change quickly.

The Nortel Boom and Bust

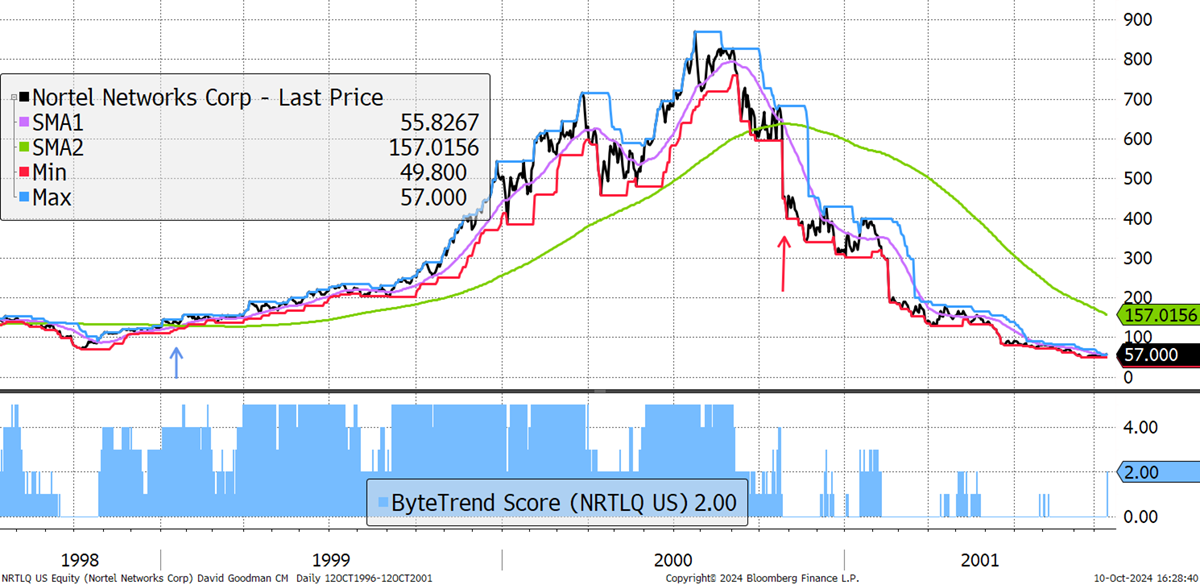

Nortel was delisted in 2015, having destroyed all of its equity capital. Yet savvy momentum investors could have picked up on Nortel in the late 1990s, as the price took off, and exited before the collapse. I can illustrate that with ByteTrend using a score of 5 for a buy and a 0 for a sell; a simple implementation of the strategy.

Nortel Price Trend

There are other ways to implement this such as buy 5, sell 2 or sell 1, but to keep it simple, I’ll start with buy 5, sell 0. If you are unfamiliar with ByteTrend, please see our guide.

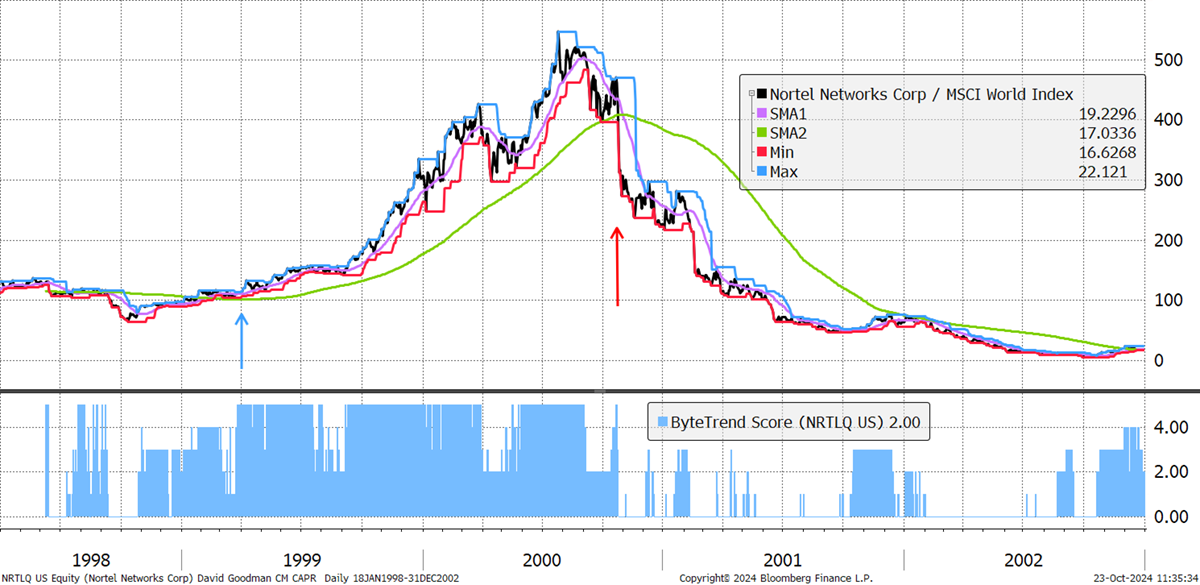

An improvement would be to use price relative instead of price, as I explained in part 2. That is the price measured relative to the stockmarket; an index such as the S&P 500 or the World. The chart becomes much cleaner, and much of the volatility disappears. By dividing the price by the market price, much of the day-to-day market noise disappears, and what’s left is whether the stock is doing better or worse than the market. With price relative, the ByteTrend score is more consistent and easier to interpret. On this occasion, the entry and exit points were similar, but at least the actions were more decisive and less open to interpretation.

Nortel Price Relative Trend

This is an extreme situation. On the way up, all is well, but the way it cracked on the way down was horrendous. Nortel was a $243 billion mega-cap stock behaving like a volatile mid-cap. Back then, this was a lot of money. I believe the world’s most valuable company at the time was Microsoft, worth $600 billion, closely followed by GE ($580 billion), which briefly held the lead. Nortel was up there (not shown due to lost data).

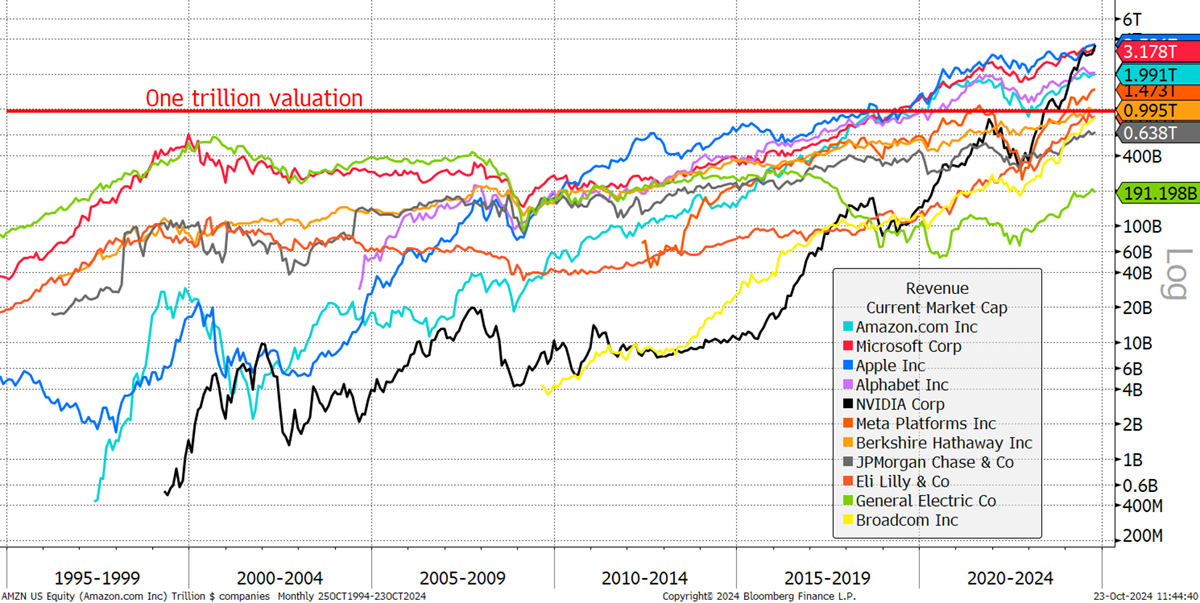

Trillion-Dollar Companies

The trillion-dollar companies never came to be in the dotcom bubble and had to wait until 2018 when Apple finally broke the glass ceiling. Today, there are six or seven trillion-dollar companies (it keeps changing) in the US, plus Saudi Aramco (not shown), which sits on vast oil reserves. There are none from China, Japan or Europe, where the most valuable companies are Tencent ($501 bn), Toyota ($431 bn), and Novo Nordisk ($538 bn), respectively.

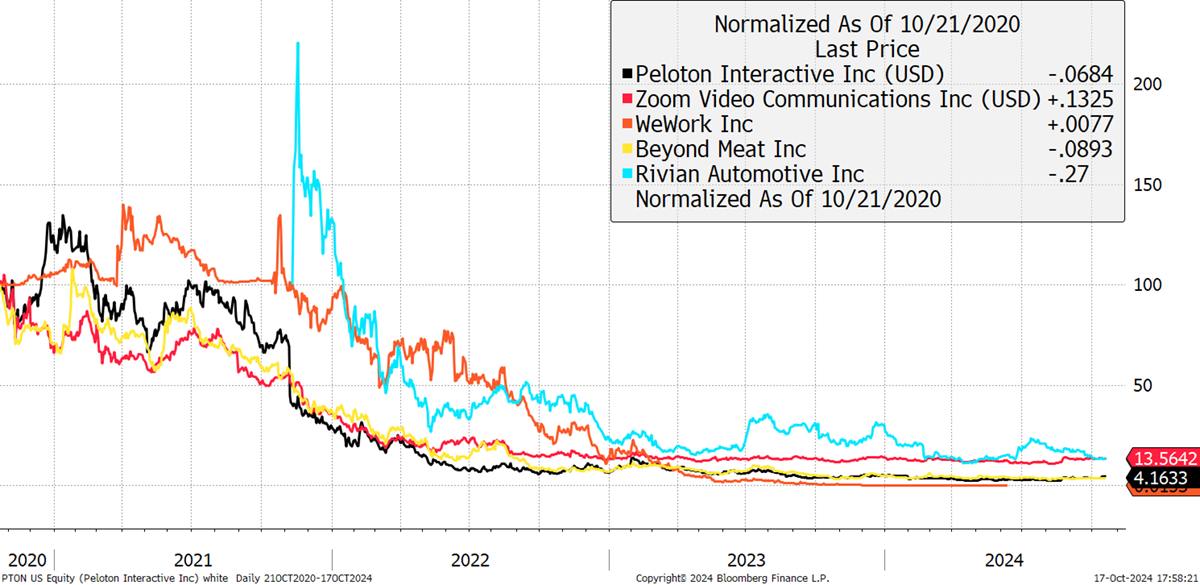

By executing a trend-following strategy, momentum investors end up owning these valuable stocks, as is highly fashionable today. But for the few that made it to the top, consider the hundreds of companies that failed. There is no shortage of examples, which may still be ongoing concerns, but the outcomes for investors have been a wipeout. For example, Zoom is highly profitable, making profits of $1.7bn per year, yet the share price still collapsed. WeWork, on the other hand, is dead and buried. I show some examples from the 2021 stockmarket bubble. Many companies slumped by 70%, 80%, 90% or even 95%. It was a shambles.

Big Names that Didn’t Make it

Most importantly, a trend-following strategy isn’t about a single company but about the market leaders, of which, at any given time, there are many. That remains true whether the market is rising or falling.

The stocks above were all momentum stocks, or market leaders, at some point. The successful momentum investor who held Nortel in a different era will also have held many stocks like it at the time. For example, in the 2021 bubble, many different investment themes rose and fell together, whether it was meme stocks, alternative energy, cloud computing, blockchain, electric vehicles, or plant-based food. They all died at the same time in a momentum crash, which I’ll look at in more detail in my next update in this series. The point is that diversification didn’t help.

You could just sell sooner, but the more the investor “tightens” the strategy, by having tighter stop losses, they end up missing the rallies. Tight constraints won’t allow the winners to run because even the strongest trends can be volatile. This tradeoff between freedoms and constraints in the investment strategy has been plaguing investors for years. There are good and bad answers, but no right answers, as what happens in the future is, unfortunately, unpredictable.

That said, diversification helps up to a point. Let’s say you limit country, sector, or theme exposure, so that if tech blows, like it did in 2000, there are other things going on in the portfolio. That will certainly calm portfolio drawdowns (losses), but there are two problems with that.

The first is that the strongest trends reside in the strongest countries and sectors. Diversifying away from them into weaker trends dampens the performance of the strategy when the aim is to milk it while you can. The other problem is that when the market goes, everything tends to go at the same time, as we saw in meltdowns such as 2008. Unless you owned lots of defensive stocks such as KO (part 2), which were not momentum stocks at the time, the winners tend to take the escalator up, and the elevator down.

The successful momentum investor knows this, as do the experienced asset allocators. The momentum investor has to make hay when the sun shines and then keep going in the drought that follows. The experienced asset allocator doesn’t bet the ranch on momentum and holds other strategies alongside, such as value and quality, combined with other asset classes and strategies. They’ll still feel pain from the inevitable momentum crashes, but with a superior long-term track record behind them because, hopefully, they’ll have banked the upside while the going was good. It is much easier to absorb pain from a position of strength than from a position of weakness.

Of course, just as one trend ends, another begins. Back in 2000, just as Nortel and the gang turned down, a long-forgotten yellow metal raised its head. Gold emerged from a 20-year bear market, having peaked in 1980 at $850. In September 2000, after a couple of false starts, gold gave a relative ByteTrend score of 5, which saw the beginning of a major bull market.

Gold Price Relative 1998 to 2002

Yet the price of gold was still falling, but it had started to outperform the stockmarket. By May 2001, gold broke out to $285, and a 10-year bull market began. By September 2011, the price peaked at $1,911.

Gold Price 1998 to 2002

In a trend-follower parlance, “ride the escalators”. As one reaches its destination, jump onto the next and repeat. It all sounds so simple, except for one thing: the momentum crash, which I will be covering next week.

A Week at ByteTree

In The Multi-Asset Investor, I looked at the lost decade, which Goldman Sach’s chief strategist, David Kostin, has recently forecasted for the US market. Kostin’s reasons are ones I have mentioned before, such as sentiment, whereby the crowd is overly bullish on equities, the economy, concentration, i.e. too few stocks dominate the market, and last but not least, valuation. Concentration risk is key because that is what has historically rung the bell. But what’s the catalyst? That’s the harder question. I also looked at the Rothschild Investment Trust aka RIT Capital (RCP). Another one not to miss.

In my monthly Atlas Pulse update on gold, Glitter or GLTER, I looked at the World Gold Council’s expected return framework for gold. A credible answer to this important question will lead to greater demand from institutional investors. They did well, and their answer helped us better understand what drives the gold price.

Finally, in crypto, Meet the Resistance reminded us that the Bitcoin miners need to be paid. High prices are met with higher payouts to the miners. Fortunately, the halvings make things easier. For example, it costs 75% less for the Bitcoin miners to sustain a price than it did at the 2017 peak and 50% less than at the 2021 peak. That’s bullish, especially over the long term, but it is important to manage expectations.

Have a great weekend,

Charlie Morris

Founder, ByteTree